Both Roth IRA and Roth 401(k) accounts are rising in popularity due to their benefit of tax-free retirement income. Our previous two-part series explained important information about these two accounts: The first article explained basic differences in their features, and the second covered contribution and distribution differences. Based on some reader questions we received, in this article we delve a bit deeper to cover the all-important five-year holding rule.

Understanding the five-year rule for Roth IRAs and Roth 401(k)s ensures that individuals avoid taxes and/or penalties on their retirement investments and successfully reap the full financial benefits of a qualified distribution.

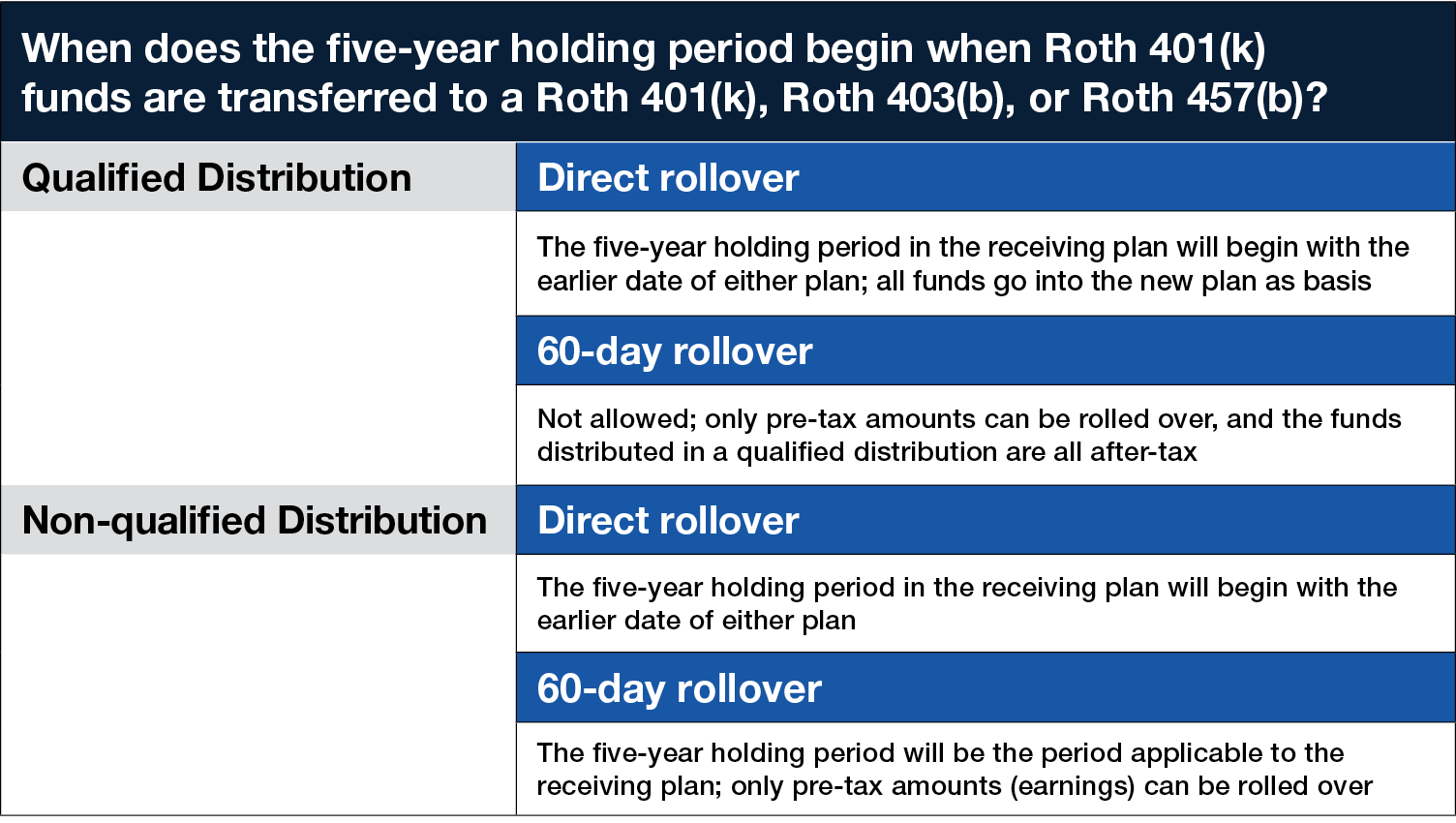

Requirements of the Five-Year Rule

“Qualified distributions” from a Roth account are income tax free. Whereas non-qualified Roth distributions may or may not be tax free. A qualified distribution requires the following:

1. An individual must hold the account for five years prior to receiving the distribution, and

2. The distribution must take place on or after the date the account owner turns age 59 ½.

The exception to this rule occurs when an account holder suffers total disability or death before an account meets these requirements. For Roth IRAs only, a distribution up to $10,000 for the purchase of a “first home” qualifies for tax-free distribution.

The Five-Year Rule for Roth IRA Contributions

To be deemed “qualified” to receive tax-free distributions from a Roth IRA, the account holder must meet the requirements of the five-year rule. The five year “clock” begins the first time funds (whether through contributions or conversion) are deposited into any Roth IRA, regardless of where an individual establishes the account. Again, for an account holder’s distributions to qualify as tax free, they must, regardless of age, have at least one Roth IRA in their name for five years. (All examples provided herein are hypothetical and do not reflect actual client experiences.)