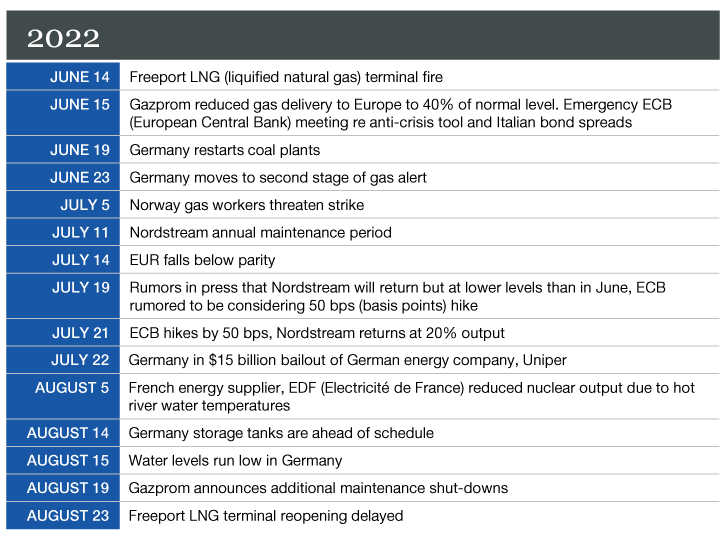

Since the onset of the Russia-Ukraine war in February 2022, Europe has been embroiled in a race to maintain energy supplies that would, under normal circumstances, originate largely from Russia. As the conflict enters its seventh month, the dimensions of the energy shock facing Europe are more fully known, and they are daunting. This more damaging phase of Europe’s economic trauma follows a series of events (see Figure 1) that have contributed to the intense volatility in European energy prices and has initiated relief measures, as European governments step in to limit the impact on consumers and industries.

Figure 1. Timeline of Events Exacerbating Europe’s Energy Crisis

Source: Lord Abbett. Data as of 08/23/2022. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment.

Gazprom’s move to reduce gas deliveries to Europe to 40% on June 15 was a regime change. It marked a new Russian strategy to stress the eurozone economically. But despite all the pressure on Europe, the region has proven resilient, although at a severe economic cost. Two symptoms of that cost are a radically smaller eurozone current account surplus and a diminished value of the euro. European growth expectations have also significantly declined. The most recent Bloomberg economic survey for the eurozone expects little growth for the region in 2023.

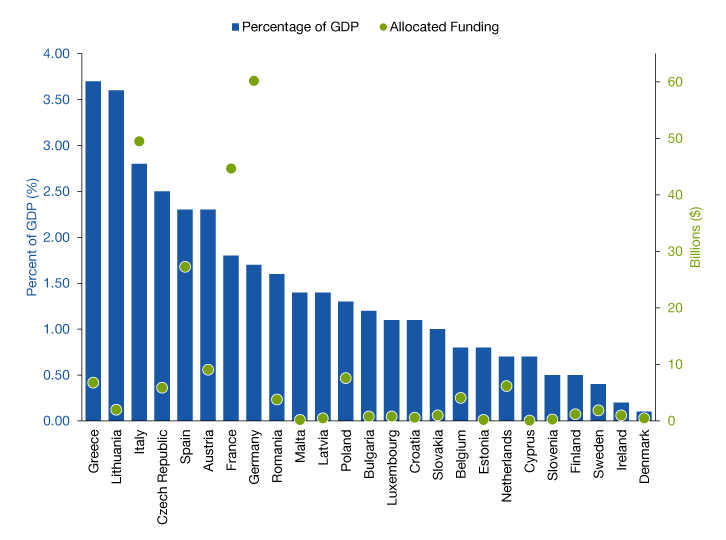

Europe’s high-starting dependency on Russian natural gas means that the process to switch energy sources will take time. The complications are numerous. Consumers face an elongated cost-of-living crisis and battered confidence. Governments are offsetting the damage with fiscal spending (see Figure 2), but they cannot forestall the negative impact indefinitely. Greece, for example, has already allocated almost 4% of GDP (gross domestic product) to energy offsets. Climate events are also exacerbating the gas shortage, as low water levels imperil transport of coal—itself a stopgap measure—while high water temperatures curtail nuclear electricity generation in France.

Figure 2. Eurozone Nations Are Spending to Cushion the Energy Shock to Consumers and Businesses

Government-allocated funding by country as a percentage of GDP and in billions of U.S. dollars (September 2021-July 2022)

Source: Bruegel, Giovanni Sgaravatti, Simone Tagliapietra, and Georg Zachmann, “National Policies to Shield Consumers from Rising Energy Prices”, August 10, 2022. Data as of 08/10/2022. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment.

High natural gas prices are also challenging business models in Europe, dampening production of energy-intensive industries like nitrogen fertilizers and aluminum. To stave off a full energy shortage, Europe is conserving energy and filling up natural gas storage tanks, but filling those tanks comes with an economic cost of reduced production from gas-dependent industries. The race to reformat energy supply also pressures Europe into more complicated relations with energy-exporting countries like Algeria, Angola, and Azerbaijan.

The policy response is playing catchup with these developments. ECB (European Central Bank) officials are signaling more aggressive rate hikes over the next year as they fret about long-term damage to inflation expectations. Rumors in the press suggest the ECB is considering quantitative tightening (i.e., reducing bond purchases) a policy move that the markets considered unlikely until recently. The EU recently announced an emergency intervention in power markets, the details of which are forthcoming but likely involve a reshaping of the region’s electricity markets. Europe is headed into a crucial period both for the conflict in Ukraine—where both sides are looking to achieve military breakout—and for the energy shortage in Europe, where the region’s leaders are looking to break through to the other side of the coming winter intact.

Investment Implications

Although valuations of European companies may seem compelling at this point, risks of further deterioration in fundamentals as costs rise, and demand declines, and the lack of any catalyst that may signal a resolution to the conflict in Ukraine or energy supplies in Europe suggest a continued investment underweight of the region.

As always, we remain attuned to the challenges facing global investment markets but view U.S.-focused businesses with less exposure to the difficulties facing European companies more favorably. Within that framework, hawkish Federal Reserve policy and high inflation in the U.S. have prompted a defensive outlook where an "up-in-quality" bias in high-quality, fixed-income portfolios may be an effective response to current market conditions.

Meanwhile, our outlook on the U.S. energy sector remains positive, as the financial conditions of these companies remains strong. As a result, we believe that spreads for energy-related companies should continue to compress versus their benchmark indexes. Thus, we are overweight energy-related companies, particularly the exploration and production sector.

More Market Insights and Resources for Investors

The ECB Steps Up Its Battle Against "Fragmentation"

Insight

Fixed Income: Finding Opportunities in the Quality and Maturity Curves

We think an “up-in-quality” bias in corporate bonds, along with capturing spread further out on the maturity curve, may serve investors well in the current environment.

About the Author

Senior Managing Director, Chief Investment Risk Officer

Jeffrey Herzog is the Chief Investment Risk Officer at Lord Abbett. In this role, he leads investment risk management, a component of the firm’s Data Driven Insights team. Mr. Herzog and the investment risk management team are responsible for continually enhancing the firm’s investment risk capabilities, including risk frameworks and analytics; performing independent investment risk oversight; constructively challenging investors’ convictions and positioning to promote risk awareness; and reporting independent risk opinions to the firm’s leadership.

Important Information

Unless otherwise noted, all discussions are based on U.S. markets and U.S. monetary and fiscal policies.

Asset allocation or diversification does not guarantee a profit or protect against loss in declining markets.

No investing strategy can overcome all market volatility or guarantee future results.

The value of investments and any income from them is not guaranteed and may fall as well as rise, and an investor may not get back the amount originally invested. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance.

Market forecasts and projections are based on current market conditions and are subject to change without notice.

Projections should not be considered a guarantee.

Equity Investing Risks

The value of investments in equity securities will fluctuate in response to general economic conditions and to changes in the prospects of particular companies and/or sectors in the economy. While growth stocks are subject to the daily ups and downs of the stock market, their long-term potential as well as their volatility can be substantial. Value investing involves the risk that the market may not recognize that securities are undervalued, and they may not appreciate as anticipated. Smaller companies tend to be more volatile and less liquid than larger companies. Small cap companies may also have more limited product lines, markets, or financial resources and typically experience a higher risk of failure than large cap companies.

Fixed-Income Investing Risks

The value of investments in fixed-income securities will change as interest rates fluctuate and in response to market movements. Generally, when interest rates rise, the prices of debt securities fall, and when interest rates fall, prices generally rise. High yield securities, sometimes called junk bonds, carry increased risks of price volatility, illiquidity, and the possibility of default in the timely payment of interest and principal. Bonds may also be subject to other types of risk, such as call, credit, liquidity, and general market risks. Longer-term debt securities are usually more sensitive to interest-rate changes; the longer the maturity of a security, the greater the effect a change in interest rates is likely to have on its price.

The credit quality of fixed-income securities in a portfolio is assigned by a nationally recognized statistical rating organization (NRSRO), such as Standard & Poor’s, Moody’s, or Fitch, as an indication of an issuer’s creditworthiness. Ratings range from ‘AAA’ (highest) to ‘D’ (lowest). Bonds rated ‘BBB’ or above are considered investment grade. Credit ratings ‘BB’ and below are lower-rated securities (junk bonds). High-yielding, non-investment-grade bonds (junk bonds) involve higher risks than investment-grade bonds. Adverse conditions may affect the issuer’s ability to pay interest and principal on these securities.

Glossary & Index Definitions

A basis point is one one-hundredth of a percentage point.

The European Central is the central bank of the 19 European Union countries which use the euro.

The Federal Reserve (Fed) is the central bank of the United States. The federal funds (fed funds) rate is the target interest rate set by the Fed at which commercial banks borrow and lend their excess reserves to each other overnight.

This material may contain assumptions that are “forward-looking statements,” which are based on certain assumptions of future events. Actual events are difficult to predict and may differ from those assumed. There can be no assurance that forward-looking statements will materialize or that actual returns or results will not be materially different from those described here.

The views and opinions expressed are as of the date of publication, and do not necessarily represent the views of the firm as a whole. Any such views are subject to change at any time based upon market or other conditions, and Lord Abbett disclaims any responsibility to update such views. Lord Abbett cannot be responsible for any direct or incidental loss incurred by applying any of the information offered.

This material is provided for general and educational purposes only. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Lord Abbett product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice.

Please consult your investment professional for additional information concerning your specific situation.

This material is the copyright © 2022 of Lord, Abbett & Co. LLC. All Rights Reserved.

Important Information for U.S. Investors

Lord Abbett mutual funds are distributed by Lord Abbett Distributor LLC.

FOR MORE INFORMATION ON ANY LORD ABBETT FUNDS, CONTACT YOUR INVESTMENT PROFESSIONAL OR LORD ABBETT DISTRIBUTOR LLC AT 888-522-2388, OR VISIT US AT LORDABBETT.COM FOR A PROSPECTUS, WHICH CONTAINS IMPORTANT INFORMATION ABOUT A FUND'S INVESTMENT GOALS, SALES CHARGES, EXPENSES AND RISKS THAT AN INVESTOR SHOULD CONSIDER AND READ CAREFULLY BEFORE INVESTING.

The municipal bond market may be impacted by unfavorable legislative or political developments and adverse changes in the financial conditions of state and municipal issuers or the federal government in case it provides financial support to the municipality. Income from the municipal bonds held could be declared taxable because of changes in tax laws. Certain sectors of the municipal bond market have special risks that can affect them more significantly than the market as a whole. Because many municipal instruments are issued to finance similar projects, conditions in these industries can significantly affect an investment. Income from municipal bonds may be subject to the alternative minimum tax. Federal, state, and local taxes may apply. Investments in Puerto Rico and other U.S. territories, commonwealths, and possessions may be affected by local, state, and regional factors. These may include, for example, economic or political developments, erosion of the tax base, and the possibility of credit problems.

The information provided is not directed at any investor or category of investors and is provided solely as general information about Lord Abbett’s products and services and to otherwise provide general investment education. None of the information provided should be regarded as a suggestion to engage in or refrain from any investment-related course of action as neither Lord Abbett nor its affiliates are undertaking to provide impartial investment advice, act as an impartial adviser, or give advice in a fiduciary capacity. If you are an individual retirement investor, contact your financial advisor or other fiduciary about whether any given investment idea, strategy, product or service may be appropriate for your circumstances.

Important Information for non-U.S. Investors

Note to Switzerland Investors: In Switzerland, the Representative is ACOLIN Fund Services AG, Leutschenbachstrasse 50, CH-8050 Zurich, whilst the Paying Agent is Bank Vontobel Ltd., Gotthardstrasse 43, CH- 8022 Zurich. The prospectus, the key information documents or the key investor information documents, the instrument of incorporation, as well as the annual and semi-annual reports may be obtained free of charge from the representative. In respect of the units offered in Switzerland, the place of performance is at the registered office of the representative. The place of jurisdiction shall be at the registered office of the representative or at the registered office or domicile of the investor.

Note to European Investors: This communication is issued in the United Kingdom and distributed throughout Europe by Lord Abbett UK Ltd., a Private Limited Company registered in England and Wales under company number 10804287 with its registered office at Tallis House, 2 Tallis Street, Temple, London, United Kingdom, EC4Y 0AB. Lord Abbett UK Ltd (FRN 783356) is an Appointed Representative of Kroll Securities Limited (FRN 466588), which is authorised and regulated by the Financial Conduct Authority.

Lord Abbett (Middle East) Limited is authorised and regulated by the Dubai Financial Services Authority (“DFSA”). The entire content of this document is subject to copyright with all rights reserved. This research and the information contained herein may not be reproduced, distributed or transmitted in any jurisdiction or to any other person or incorporated in any way into another document or other material without our prior written consent. This document is directed at Professional Clients and not Retail Clients. Any other persons in receipt of this document must not rely upon or otherwise act upon it. This document is provided for informational purposes only. Nothing in this document should be construed as a solicitation or offer, or recommendation, to acquire or dispose of any investment or to engage in any other transaction. Nothing contained in this document constitutes an investment, an offer to invest, legal, tax or other advice or guidance and should be disregarded when considering or making investment decisions.